Australians have some of the highest amounts of debt in the Western world. What can you do to manage your own debt?

Credit cards, zero per cent balance transfers, lines of credit, interest-free store loans…it really has never been easier to spend money that you haven’t yet earned. Throw in low interest rates and a solid economy with few real hiccups for the best part of two decades and you have ripe conditions to encourage a binge on debt of epic proportions. And that’s exactly what we have witnessed.

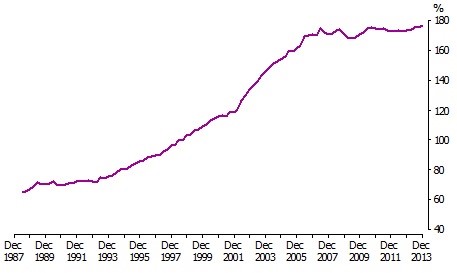

SIZE OF HOUSEHOLD DEBT COMPARED WITH ANNUAL INCOME

Source: Australian Bureau of Statistics

The above chart shows the steep upward trajectory of the level of debt held by Australians. On average, people have three times as much debt in proportion to their income compared with 25 years ago. This trend has been reinforced by a recent Bankwest Curtin Economics Centre study.

Debt is clearly no longer a dirty word in the minds of many Australians. Additionally, saving a reasonable deposit for a first home is becoming more and more out of reach for young people, so many are taking the situation up a notch and turning to credit cards and personal loans to raise enough money for the deposit. A recent edition of the Genworth’s Homebuyer Confidence Index report stated that almost one in five first home buyers (19 per cent) is using a credit card to help fund their house deposit!

Whilst the banks are having a field day providing all this credit, it does pose some serious risks if the situation were to take a turn for the worse. If you have borrowed heavily with little equity in your home, it leaves you with little buffer to ride out a tough period or an unforeseen event. The sudden loss of a job or a serious illness of a family member could place significant stress on the household and impact upon your ability to maintain repayments. A small decline in house value (yes, it can happen) could see you in a position where your home value is less than your mortgage.

Managing debt

So what steps can you take to manage your debt burden?

Focus on behaviour change

Instead of focusing purely on things such as loan types and interest rates, concentrate on establishing the right behaviours. This includes knowing exactly where your money is coming from and going to. After all, you can’t manage what you don’t measure. It’s a simple thing, but few people can confidently state how much they are spending on groceries, bills or discretionary items.

Use a spreadsheet or one of the many online budget/money trackers to start measuring your outgoings. If you’re not a fan of technology, the old envelope system will work just fine.

Repayment plan: Debt snowball versus debt avalanche

Where you have multiple personal debts such as credit cards, personal loans etc., it’s useful to have a plan of attack in terms of what you pay and when.

Two common methods used are the ‘debt snowball’ and ‘debt avalanche’.

The ‘debt snowball’ method involves paying your smallest debts first to create positive momentum. As human beings, we like to feel that we are making progress. As you finish repaying each debt, you remove it from your list and this helps to simplify things and reduce stress. In practical terms, this means paying off items such as credit cards first before progressing onto larger debts.

The ‘debt avalanche’ method focuses on paying off the debt with the highest interest rate first. Debts with a higher interest rate grow faster due to the effect of compounding interest. So, paying these debts first should save you more money in the long run.

From a purely financial standpoint, the ‘debt avalanche’ method is less costly than the ‘debt snowball’ method in general. But for people that need the extra motivation and feeling of progress, the ‘debt snowball’ method may be a better option.

Be aware of the debt consolidation trap

Debt consolidation may sound like a viable option for repaying your debt because of a lower interest rate and regular repayment amount. For example, replacing your credit card debt with a personal loan can greatly reduce the interest bill. However, often the reason the regular repayment amount is lower is because the term of the loan is extended. So a longer period to repay means a lower regular repayment, but you could actually end up paying more if you’re not careful.

If you’ve consolidated your credit and store cards, make sure you immediately cut up the cards to avoid the temptation to use them and rack up further debt. Also, devise a realistic time frame in which to repay the debt. This needs to be manageable and practical so that it is achievable.

Put the letters regarding credit limit increases straight in the bin!

We’ve all received letters in the mail offering credit limit increases for a credit card or loan.

It may seem like a harmless exercise to accept one of these offers which can provide you with extra flexibility when required. However, the reality is that if funds are available, you are more likely to use that extra credit. An increased limit just gives you more opportunity to spend money you don’t have.

Should you really have a line of credit?

A line of credit secured against your home may sound good in theory. This is a flexible credit facility with a low interest rate and in most cases it has no set repayments. It basically works like a gigantic credit card that only requires you to pay the interest at the end of each month. Some lenders will even allow you to capitalise the interest, meaning that the interest amount just gets added onto the loan balance each month.

These facilities are popular these days as they allow you to access the equity in your home (the difference between the house value and the mortgage balance) without needing to sell the property. The problems arise when you start using these funds for everyday expenses and even holidays and other nice-to-haves without a clear picture as to a) whether you can afford these items and b) how you will ever repay the total amount.

Final word

Debt is just a symptom of a bigger problem, which is spending more than you earn. Things such as consolidating the debt or fancy credit facilities won’t help your situation if you don’t address the root of the problem. This means knowing exactly what comes in and out of your bank account and putting an achievable plan in place to monitor your progress and tackle the debt.